Fed Roulette

Predicting the FOMC’s latest half-point rate cut resembled a game of roulette.

Select audio playback for easy listening of our latest RWA report.

Predicting the FOMC’s latest half-point rate cut resembled a game of roulette. The stakes proved high, with betting odds averaging typical 50-50 coin-flip odds. However, hours before the decision, the probability of a 50bps September rate cut jumped to 75%. Recall that market expectations had polarised (Figure 1), following August’s stickier CPI and fragile jobs data, marked by the second worst revision in US history.

Unprecedented divergences emerged, with most economists (101/118) favouring a 25bps cut, juxtaposed with record leveraged bets by traders for 50bps, based on a Bloomberg survey & Fed Fund Futures data (Figure 2).

Akin to betting red or black on a roulette wheel, trading ahead of the FOMC decision hasn’t proved this edgy in a generation. Analysis by Deutsche Bank AG’s Jim Reid shows the gap in the realised surprise of Fed Funds Rate vs. market pricing two days before the meeting was the largest in over 15 years (Figure 3). This event risk offers powerful cross-asset behavioural inflection point, spotlighted in our latest client report.

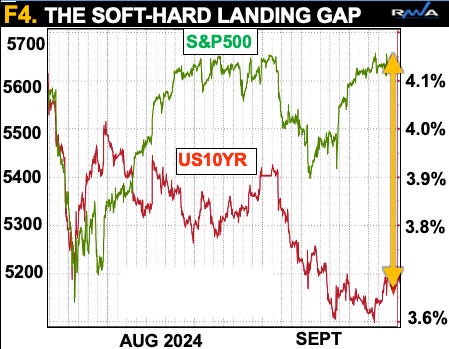

Looking back at the record timeline, it also serves as a precarious historical echo rhyme of both the event risks of 2007-08 GFC and 2000 TMT, reminding us of what happens when the Fed forces such a tight policy for too long (Figure 4). Will Fed policy once again lag “behind the curve”?

Mr. Market remains elusive as ever, with stocks and bonds appearing to be sending conflicting signals about the economy’s forward trajectory (Figure 4). S&P500 made a new all-time intraday high at 5689.75, supercharged by the recent lunar eclipse, having recovered from the August flash-crash. Fuelling this rally was a revived “soft-landing” consensus at record extremes. Meanwhile, bond prices rallied and yields plummeted, notably shorter-term rates.

Consequentially, the 10-2 year yield curve, which has been “inverted” since July 2022, for a record 770 days, has now rapidly “un-inverted,” seeming to imply a looming recession (Figure 6). It’s noteworthy, that the only other occurrences in the past century of a 500+ day inversion were in 1929, 1973-74 and 1978-80, which all lead to market shocks.

Our timing models remain on alert, notably the FSC LT model which continues to signal a major topping process into 2025. In macro terms, a bout of US negative surprises continues to weigh - GDP slowdown, sticky inflation & fragile labour data - (Figure 7). This is further recently pressured by broader global concerns of depressed oil prices and weak China data.

What about the path of rates? US10YR is developing an inflection point, after completing its summer decline into a nearby support zone at 3.54-30%, then resuming back higher for longer, as part of the long-term Kondratieff wave (Figure 8).

Think 1970s inflation resurgence, another historical analogue that remains on track, based on a pattern of rolling waves of volatility (Figure 6). Our base- case scenario could lead to a two-stage pattern of an inflation fall (stagflation), likely coinciding with a market shock, preceded by a multi-year rise.

Meantime, long-term cross-asset analysis still warns that commodities are verging on a new super bull cycle. In behavioural terms, it’s time to prepare for switch from FOMO to FOLO (Fear of losing out). Read previous RWA report for more details. Risk management is paramount in both the market and the casino game. Bon chance!